IRS proposed regulations and a related revenue ruling clarify the type, timing, and tax deferral provisions for maximizing the tax benefits of a Qualified Opportunity Zone (Zone) investment. The earlier a taxpayer invests in a Zone, the greater potential step-up in tax savings.

The IRS issued proposed regulations and a related revenue ruling addressing the treatment of new investments in a Qualified Opportunity Zone (Zone), a tax incentive program mandated in the Tax Cuts and Jobs Act (IRC Sec. 1400Z-1 and 1400Z-2). The guidelines clarify the type of gains that may be deferred and invested in Zones; time frames for investing gains and obtaining tax benefits; rules addressing the tax deferral, and more.

The IRS issued proposed regulations and a related revenue ruling addressing the treatment of new investments in a Qualified Opportunity Zone (Zone), a tax incentive program mandated in the Tax Cuts and Jobs Act (IRC Sec. 1400Z-1 and 1400Z-2). The guidelines clarify the type of gains that may be deferred and invested in Zones; time frames for investing gains and obtaining tax benefits; rules addressing the tax deferral, and more.

Zone investments offer both a temporary deferral and partial exclusion of taxable gains in exchange for investing in a low-income community or Zone. Taxpayers have 180-day window to invest a gain in a Zone to qualify for deferral.

With the type, timing, and tax deferrals set in the proposed rules, it’s a good time for investors to work with their advisors to time a sale or exchange that triggers a gain to get the greatest tax benefits from Zone investments. The gain must be recognized on the earlier of i) the date on which the investment is sold or exchanged, or ii) Dec. 31, 2026, to maximize the length of the deferral and incentives. Taxpayers that miss the 8-year window can still elect the permanent exclusion if the investment is held longer than 10 years.

Greater clarity

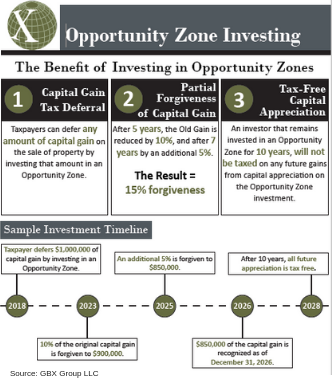

The program encourages taxpayers to invest in underfunded communities (see New in 2018: Opportunity Zone Investments) by providing them with three tax incentives.

- Defer recognizing a capital gain for up to eight years for gains re-invested in a Zone. Deferred gains will be recognized either when Zone interest is sold or, at the latest, December 31, 2026. This means the earlier you invest in a Zone, the greater the tax savings.

- Exclusion of up to 15 percent of original gain when the Zone investment is held for specified time periods.

- An exclusion of the gain eventually recognized from Zone investments that are held for at least 10 years.

The proposed regulations clarify who is an eligible taxpayer and who isn’t. Individuals, partnerships, corporations, estates, trusts and others are eligible taxpayers.

The proposed regs further provide that only capital gains invested in a Qualified Opportunity Fund (Fund) are eligible for tax deferral. Qualifying funds are any partnership or C corporation organized to make investments in Zone property. Investors must reinvest gains in a Fund within 180 days of the recognized gain to qualify for a tax deferral. In turn, the Fund must hold at least 90 percent of its assets in Zone stock, partnership interests, or property.

What’s the savings

Tax savings step-up based on how long the Fund investment is held.

- Investors who hold their Fund investment for five years can see 10% of the deferred gain permanently excluded.

- Holding the investment for seven years would exclude another 5% of the deferred gain.

- Investments held for at least 10 years qualify to increase their basis to the fair market value of the investment on the date it is sold, meaning none of the appreciation beyond the deferred gain is recognized as long as the investment is sold before December 31, 2047.

Timing the investment

Taxpayers with capital gains from a sale occurring between December 22, 2017 and January 1, 2027 should consider this tax saving investment. The earlier, however, a taxpayer invests in a Zone, the greater the potential step-up in tax savings.

Time a Zone investment to get the most out of these tax savings. If you are a taxpayer with a large capital gain in 2018 or expect a gain before January 1, 2027, let’s sit down and see whether the timing of this investment vehicle might be right for your portfolio.

IRS Resources

Source: Treasury, IRS issue proposed regulations on new Opportunity Zone tax incentive

IRS Opportunity Zones Frequently Asked Questions

More information on Opportunity Zones is on the Tax Reform page of IRS.gov.

Click here for complete list of Opportunity Zones.

Follow Us on LinkedIn

Photo by rawpixel on Unsplash

This commentary on this website reflects the personal opinions, viewpoints and analyses of the Wambolt & Associates employees providing such comments, and should not be regarded as a description of advisory services provided by Wambolt & Associates or performance returns of any Wambolt & Associates Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this website constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Wambolt & Associates manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Wambolt & Associates provides links for your convenience to websites produced by other providers or industry related material. Accessing websites through links directs you away from our website. Wambolt & Associates is not responsible for errors or omissions in the material on third party websites, and does not necessarily approve of or endorse the information provided. Users who gain access to third party websites may be subject to the copyright and other restrictions on use imposed by those providers and assume responsibility and risk from use of those websites.